We have been hammered by high inflation — should your retirement plans change?

By Deborah Jeanne Sergeant

You don’t need to read a news story to realize that it costs more to shop for groceries and fill your gas tank than it did a few years ago.

You don’t need to read a news story to realize that it costs more to shop for groceries and fill your gas tank than it did a few years ago.

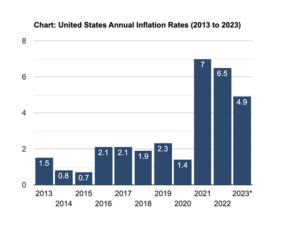

Although the current inflation rate of 4.9% (according to the Bureau of Labor Statistics) represents a decrease since 2022, it is still comparable to 2021’s average. And, it is higher than the averages of 2020, 2019, 2018, 2017 and 2016 (see chart with this story).

With the exception of 2022, the current rate is the highest the inflation rate has been since 1990 (6.1%). The trend indicates that inflation is not going back to pre-pandemic levels.

Does that mean you should adjust your retirement plan accordingly?

Randy Ziegler, certified financial planner and private wealth adviser in Oswego with Ameriprise, says no.

“We’re always factoring inflation into our calculations,” he said.

He bases retirement plans on a 4% inflation rate, even though the Federal Reserve targets between 2.5% and 3%. A long-term plan based on that much wiggle room should suffice over the long term, even when years like 2022 pop up.

“We’ve seen a little easing in a few of the price increase areas,” Ziegler said. “I don’t think people should change their basic risk tolerance because of inflation. Historically, the market makes those adjustments. If you have a balanced approach, you still have a decent amount of equity. A higher inflation rate drives a higher return. Our real returns have been pretty similar over the past 10-12 years.”

He counsels clients to remain patient and not shift their retirement money to higher risk investments because “the current inflation is likely temporary because the Federal Reserve is slowing down the economy to squeeze out that inflation pressure.”

It’s also likely that those in the later stages of their retirement will see expenses for things like travel and entertainment plateau.

Mary Tone Rodgers, chartered financial analyst who holds a doctorate of professional studies and teaches at SUNY Oswego, said that retirees should plan for 2% inflation annually. She pairs two strategies for planning for cost increases.

“Set yourself up so your retirement income can increase and plan ahead for managing your expenses,” Rodgers said. “The traditional, most conservative way to plan for increase in income is a ladder of CDs that are FDIC insured.”

When each CD matures, it rolls over to a higher interest CD. She’s also a fan of dividend growth mutual funds. Not FDIC insured, the principal value can increase or decrease, so they’re not for the risk adverse. Although these tend to increase by 6% on average annually, it’s not guaranteed.

“Last year, with a 10% increase, that was much better than average,” Rodgers said.

The past few years have been rough for those who have already retired, as last year’s tanking stock market and high inflation “had a double effect,” said Cynthia Scott, financial adviser and owner of OMC Financial in Syracuse. “Their spending power is down and their retirement savings is down. They’re in a terrible situation.”

She said that becoming more aggressive with quality stocks may help, as well as not relying as much on low-interest vehicles like CDs and savings accounts.

“Inflation eats into that interest rate,” Scott said. “That’s why they have to relook at how much they put into savings, which may not be the best place for them to put their money. We always encourage people to take a lump sum for their pension if they can. Those who get a monthly income, it’s fixed and hurt by inflation as well. If you get the lump sum, you can invest it and counter inflation as you have control of your investments.”

Those who have not yet retired may need to reconsider when and how they retire. Retiring later offers the highest Social Security payout and gives them more years of earnings. Their post-retirement lifestyle may not be as high-end as they would like.

When Scott first started financial management, she advised that people invest in treasury and municipal bonds. They have enjoyed good returns years later with 16% returns.

“Bonds lock that money in place,” Scott said.

Eric Kingson, professor in the school of social work at Syracuse University, has served on the staff of two presidential commissions examining Social Security.

“The one asset you have that’s protected against inflation is Social Security,” Kingson said. “The automatic cost of living adjustment is a very important feature of the program, assuring what money you get in the monthly benefit when you start will maintain the roughly same purchasing power as long as you live. I don’t view it as a benefit increase, but an adjustment that enables people to maintain the purchasing power of their Social Security.”

Retirees receive a more than $1,800 on average in benefits per month.

Kingson also promotes waiting until age 70 to retire to receive 124% of the full benefit. The eligibility age of 67 garners retirees 100% of the benefits. Retiring before this can dock the benefits significantly.

“It’s not unusual today for people to delay when they retire,” Kingson said. “A lot of people accept benefits but aren’t retired. If people have health and a job and they’re worried about continuing their standard of living, to the extent that they can and want to, they can expand work until things get better.”